OPERATIONS MANAGEMENT

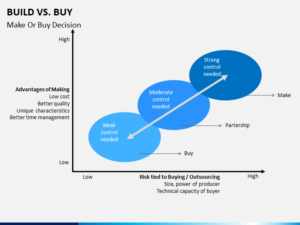

MAKE OR BUY DECISIONS

- Make or Buy Decisions is the determination whether to produce component internally or to buy it from the outside supplier.

- The decision is based on the cost.

- The cost for both the alternatives should be calculated and the alternative with less cost is to be chosen.

CRITERIA FOR MAKE:

- The product can be made cheaper by the firm.

- The finished product is being manufactured only by limited firms.

- The part needs extremely close quality control.

- The part can be manufactured from the existing facilities with experienced operators.

- The quantities are too small and/or no supplier is interested or available in providing the goods.

- Quality requirements may be so exacting or so unusual as to require special processing methods that suppliers cannot be expected to provide.

- There is greater assurance of supply.

- It is necessary to preserve technological secrets.

- It helps the organization obtain a lower cost as the purchase option is too expensive.

- It allows the organization to take advantage of or avoid idle equipment and/or labor.

- It ensures steady running of the corporation’s own facilities, leaving suppliers to bear the burden of fluctuations in demand.

- It avoids sole-source dependency.

- Competitive, political, social or environmental reasons may force an organization to make even when it might have preferred to buy.

- The distance from the closest available supplier is too great. • A significant customer required it.

- Future market potential for the product or service is expanding rapidly and forecasts show future shortages in the market or rising prices.

CRITERIA FOR BUY:

- High investments required for making.

- Does not have facilities for making.

- Skilled workers not available.

- Demand is either temporary or seasonal.

- Patent or legal formalities prevent from making the product.

- The organization may lack managerial or technical expertise in the production of the items or services in question.

- The organization lacks production capacity.

- Certain suppliers have built such a reputation for themselves that they have been able to build a real preference for their component as part of the finished product.

- The challenges of maintaining long-term technological and economic viability for a non core activity are too great.

- A decision to make, once made, is often difficult to reverse.

- It assures cost accuracy.

- There are more options in potential sources and substitute items.

- There may not be sufficient volume to justify in-house production.

- Future forecasts show great demand or technological uncertainty and the firm is unable or unwilling to undertake the risk of manufacture.

- A highly capable supplier is available nearby.

- The organization desires to stay lean.

- Buying outside may open up markets for the firm’s products or services.

- It provides the organization with the ability to b ring a product or service to market faster.

- A significant customer may demand it.

- It encourages superior supply management expertise.

CONSIDERATIONS WHICH FAVOR MAKING:

- Cost considerations (less expensive to make the part).

- Desire to integrate plant operations.

- Productive use of excess plant capacity to help absorb fixed overhead.

- Need to exert direct control over production and/or quality.

- Design secrecy required.

- Unreliable suppliers.

- Desire to maintain a stable work force (in periods of declining sales).

CONSIDERATIONS WHICH FAVOR BUYING:

- Limited production facilities.

- Cost considerations (less expensive to buy the part).

- Small volume requirements.

- Suppliers’ research and specialized know-how.

- Desire to maintain a stable work force (in periods of rising sales).

- Desire to maintain a multiple source policy.

- Indirect managerial control considerations.

- Procurement and inventory considerations.

RELATED VIDEOS FOR MAKE OR BUY DECISIONS:

https://www.myaccountingcourse.com/accounting-dictionary/make-or-buy-decision